CIBIL Score: A Thermometer for the Common People, Ignored for the Elite

CIBIL Score: Double Standard in India’s Financial System: Favouring the Wealthy While Burdening Common Citizens.

Last year, a friend from Pune called me urgently asking for money. His wife had been hospitalized, but he had already paid the bills with his credit card. He was worried about his CIBIL score because he couldn’t pay his credit card EMIs on time. Shocked, I asked, “Are you more worried about your CIBIL score than your wife’s health?” He confirmed, highlighting the undue pressure of maintaining a good credit score.

I questioned, “What’s the CIBIL score of Nirav Modi, Mehul Choksi, and Vijay Mallya? This situation reminded me of a stark contrast. While my friend worried about his CIBIL score, notorious defaulters like Nirav Modi, Mehul Choksi, and Vijay Mallya had no such concerns. Their massive defaults haven’t seemed to impact their ability to secure funds.

Take Ritu (name changed), for instance. She took a personal loan during the lockdown and paid her EMIs diligently, except for a few delays. When she needed another loan due to medical reasons, every bank rejected her application due to her low CIBIL score. She had to borrow from a relative to meet her urgent needs.

Similarly, Prakash borrowed Rs 20,000 from an online loan app on Google Play Store. Due to an accident, he delayed an EMI of Rs 3,200 by six days. The app’s team harassed him and his references, threatening to visit his home if the payment was not made immediately.

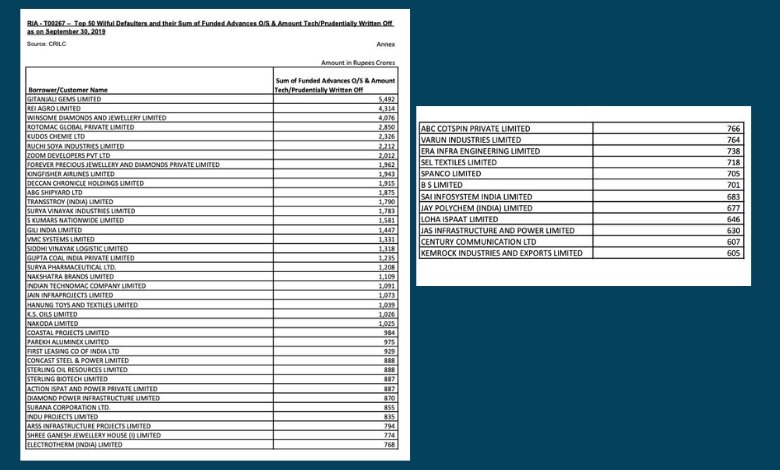

Every day, countless common citizens, small business owners, and startups have their loan applications rejected due to low CIBIL scores, often resulting from minor delays in EMI payments. This reality contrasts sharply with how large defaulters are treated. For example, India’s top 50 bank loan defaulters accounted for loans worth Rs 68,607 crore being written off until September 2019. This list includes absconding diamantaire Mehul Choksi and fugitive businessman Vijay Mallya. Recently, Yes Bank’s Asset Reconstruction Company, JC Flowers, waived off Rs 5,000 crore worth of loans to Zee Group’s Chairman Subhash Chandra Goenka, reducing his liability from Rs 6,500 crore to Rs 1,500 crore.

Social activist and Rajya Sabha Member (TMC) Saket Gokhale filed an RTI request asking for the list of the top 50 loan defaulters until February 16, 2020. In response, the Reserve Bank of India (RBI) revealed that Rs 67,078 crore had been written off by 30th Sept 2019. It is likely that many, if not all, of these defaulters have secured new loans from the banks. What about their CIBIL scores?

Congress leader Jairam Ramesh highlighted that banking frauds increased 17-fold from ₹34,993 crore in 2005-14 to ₹5.89 lakh crore in 2015-23. Between 2017-18 and 2021-22, banks wrote off loans worth ₹10 lakh crore.

On June 8 2023, the RBI issued instructions under the ‘Framework for Compromise Settlements and Technical Write-offs,’ allowing banks to settle or write off accounts of willful defaulters and fraudsters, permitting them to take new loans after a 12-month cooling period. This raises questions about the double standards in the Indian financial system. While common citizens struggle to get loans for emergency needs due to low CIBIL scores, wealthy defaulters can reapply for loans after massive write-offs.

It seems CIBIL is a thermometer that only checks the temperature of common people, failing when it comes to the rich or politically influentials. The disparity between how common citizens and wealthy defaulters are treated by the Indian financial system is not just absurd; it’s a clear reflection of a deeply entrenched double standard that favors the elite.